Enhanced premium tax credits (ePTCs), first introduced as part of the American Rescue Plan Act in 2021, have made ACA Marketplace coverage more affordable for the millions of enrollees that receive them. Enhanced tax credits have lowered the share of household income ACA Marketplace enrollees are expected to contribute out-of-pocket toward the premium payment for a benchmark silver plan. For those already eligible for premium subsidies, ePTCs have increased the total amount of tax credits the enrollee receives, while middle-income enrollees making above 400% of poverty ($62,600 for an individual enrolled in coverage for plan year 2026) have become newly eligible for the tax credits. The ePTCs were extended until the end of 2025 by the Inflation Reduction Act.

This data note compares how the out-of-pocket portion of premiums would differ if the ePTCs expire, or become extended, for select scenarios. (To produce your own estimate of how premium payments would differ compared to if the enhanced tax credits become unavailable, KFF provides an interactive tool where users are able to input their desired geography, income, and family size).

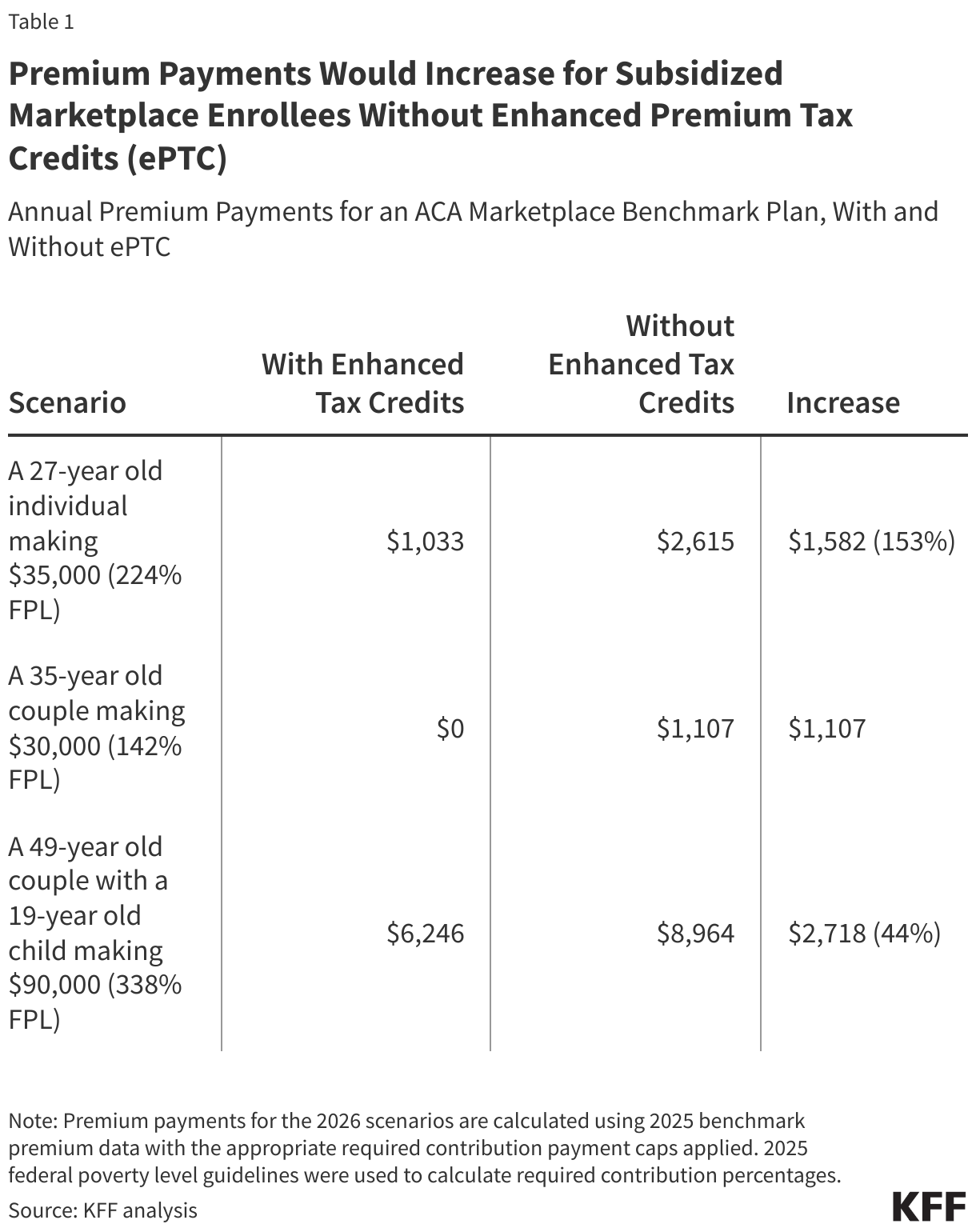

If enhanced premium tax credits expire, subsidized ACA Marketplace enrollees can expect their out-of-pocket premium payments to rise substantially. For example, a 27-year-old making $35,000 (224% of poverty) would pay $1,033 annually for a benchmark silver plan in 2026 with the ePTCs. Without the enhanced tax credits, however, they will pay $2,615 – a $1,582 (153%) increase.

With the enhanced tax credits in place, Marketplace enrollees making between 100%-150% of the federal poverty level are eligible for a fully subsidized benchmark plan. Prior to the availability of the ePTCs, enrollees making just above the poverty level were expected to contribute about 2% of their household income towards a benchmark plan. If the enhanced tax credits expire, low-income enrollees who are currently paying $0 for a benchmark plan will have to start paying for coverage again. For example, a 35-year-old couple earning $30,000 can expect to start paying $1,107 annually for a Marketplace benchmark plan.

What happens if premiums rise substantially in 2026?

There are two ways of thinking about premiums in the ACA Marketplaces. First, there is the net premium, which is what the enrollee pays out-of-pocket after taking into account their tax credit. Second, there is the gross premium, which is the amount the insurance company charges (part of which is paid by the federal government and part of which is paid by the enrollee). The expiration of the enhanced premium tax credits will affect the net premium directly (as enrollees receive less financial assistance) and it will also indirectly affect the gross premium insurers charge.

A KFF analysis of rates (gross premiums) proposed by Marketplace insurers for the 2026 plan year found that insurers are requesting a median increase of 18% in their rates. Insurers cited several reasons for these rate increases, including that they anticipate that some healthier members will leave the ACA Marketplaces once their net (or, out-of-pocket) premium payments increase if the ePTCs expire. This results in an enrollee base that is less healthy and more expensive, on average. Insurers say that rates are rising by about 4 percentage points more than they otherwise would, due to the expiration of the enhanced premium tax credit.

If enhanced premium tax credits expire, enrollees with incomes between the poverty level and four times the poverty level will continue to be eligible for financial assistance – they will just receive a smaller tax credit than they currently do. As shown in the examples above, these enrollees will pay significantly more for their monthly premium, but they will still pay a certain percent of their income for the benchmark silver plan. In other words, the increase in their monthly premium will primarily be a result of a smaller tax credit — the amount subsidized enrollees pay is largely shielded from increases in the amount insurance companies charge.

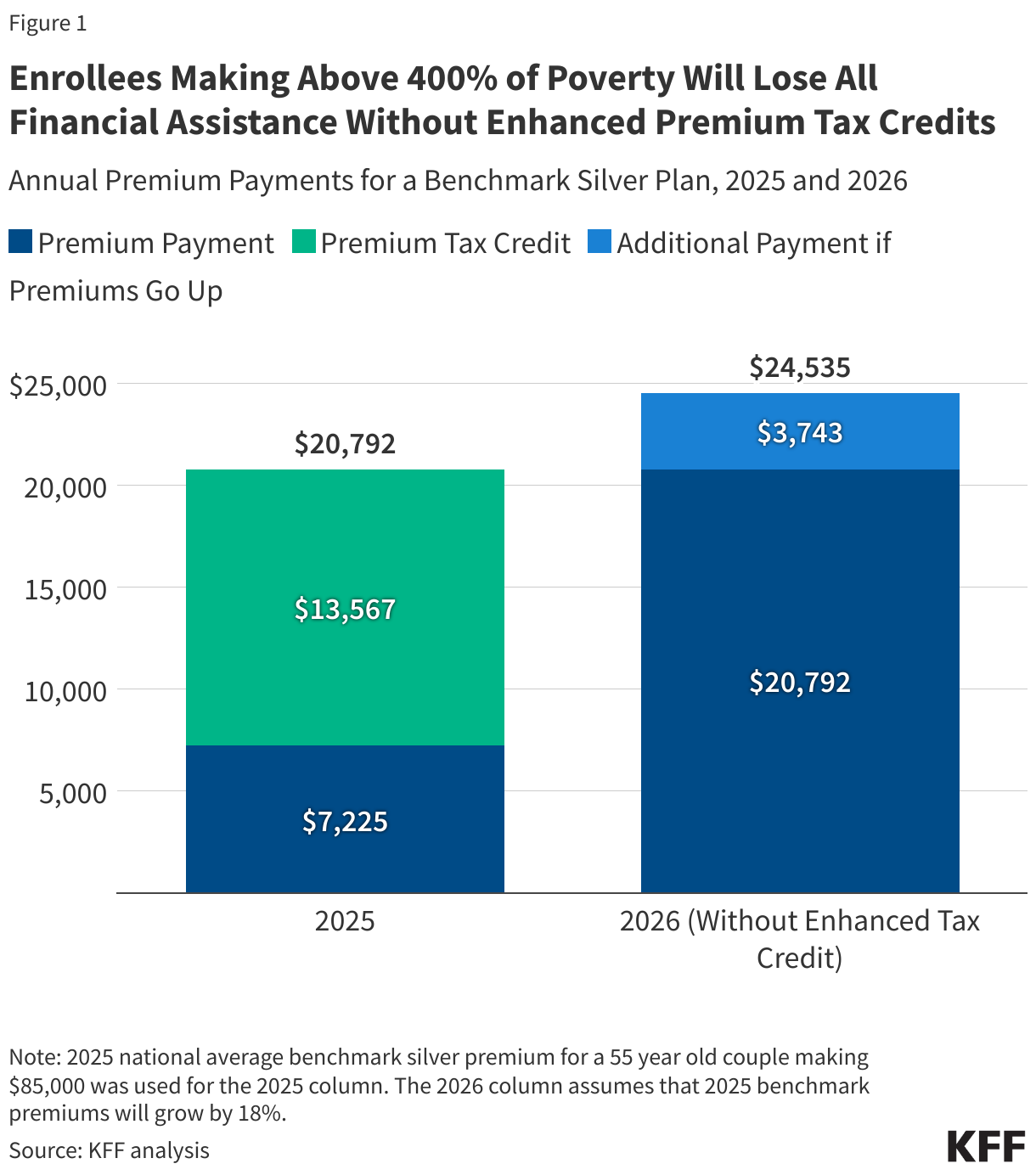

However, if enhanced premium tax credits expire, people with incomes over four times the poverty level will no longer be eligible for any financial assistance. Because their monthly payments will no longer be tied to a certain percentage of their income, these enrollees will not only lose financial assistance but will also be exposed to any increase in underlying gross premiums. With the enhanced tax credits, middle-income enrollees making above 400% of poverty currently have their out-of-pocket premium payments for a benchmark plan capped at 8.5% of their income. However, if the ePTCs are not renewed, these enrollees will experience a “double whammy” – losing their eligibility for Marketplace premium tax credits and facing the annual increases in the cost of a Marketplace plan.

On average, a 55-year-old couple making $85,000 is currently receiving $13,567 in premium tax credits annually, covering 65% of the total cost of a benchmark plan. If the ePTCs expire, this couple would lose financial assistance and pay the full annual cost of $20,792, assuming premiums stay the same. However, if the gross premium grows at a rate of 18% into 2026, the 55-year-old couple can expect their net (out-of-pocket) premium payments to more than triple if ePTCs expire, increasing by $17,310 (240%), from $7,225 to $24,535 annually for the same plan.

How do Trump Administration Regulations Affect Premium Payments?

The maximum household required contribution for a benchmark ACA Marketplace plan is indexed annually to adjust for growth in premiums relative to income. Since the introduction of enhanced premium tax credits, new (and more generous) required contribution levels for premiums were implemented without annual adjustment.

As the ePTCs are set to expire, the IRS has released the required contributions for 2026. The Trump administration introduced changes in the calculation of required contribution through the Marketplace Integrity and Affordability rule earlier this year. Compared to the indexing methodology in place previously, the maximum out-of-pocket contribution for benchmark premiums for those that receive premium tax credits has increased as a share of income.

Prior estimates indicated that in 2024, out-of-pocket premium payments among subsidized enrollees would have been over 75% higher without the enhanced tax credits. Enrollees could expect to pay even more in 2026, on average, due to annual increases in the average costs of premium and IRS changes to the contribution requirements.

Methods

Premium data for 2025 is used in table 1 as rates for 2026 have not yet been finalized. Premium data for 2025 were obtained from Centers for Medicare and Medicaid Services (CMS), insurer rate filings, and information directly received or collected by KFF researchers from state exchanges or insurance departments. To isolate the effect on premiums without enhanced tax credits in table 1, the maximum required contribution was calculated using the federal poverty threshold for 2025, comparing the applicable percentage under the IRA to what is expected for 2026. In figure 1, the 2025 scenario reports values using required contribution and poverty guidelines in place for plan year 2025. An additional 18% increase is applied in the 2026 (without enhanced tax credit) scenario to model annual increases in premiums.