Affordable Care Act (ACA) enhanced premium tax credits are set to expire at the end of this year. Enhanced premium tax credits were introduced in 2021 and later extended through the end of 2025 by the Inflation Reduction Act. The enhanced tax credits both increased the amount of financial assistance already eligible ACA Marketplace enrollees received as well as made middle-income enrollees with income above 400% of federal poverty guidelines newly eligible for premium tax credits.

Since the introduction of the enhanced premium tax credits, enrollment in the Marketplace has more than doubled from about 11 to over 24 million people, the vast majority of whom receive an enhanced premium tax credit. If enhanced tax credits expire, many Marketplace enrollees will continue to qualify for a smaller tax credit, while others will lose eligibility altogether and be hit by a “double whammy” of losing their entire tax credit and being on the hook for rising premiums.

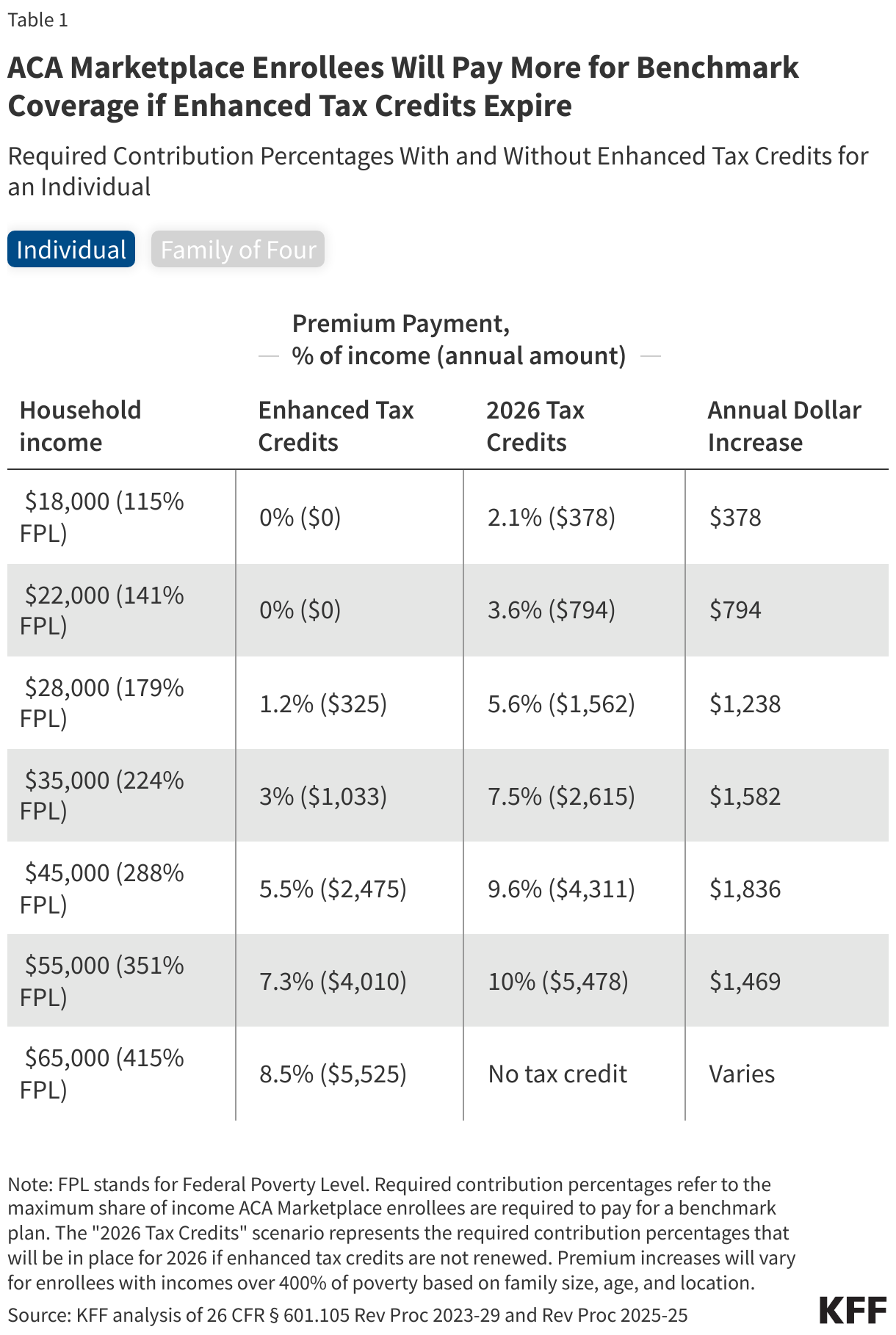

Since 2014, the ACA has capped how much subsidized enrollees pay for their health insurance premiums at a certain percent of their income, on a sliding scale, with the federal government covering the remainder in the form of a tax credit. Enhanced tax credits work by further lowering the share of income ACA Marketplace enrollees pay for a plan. For example, with the enhanced tax credits in place, an individual making $28,000 will pay no more than around 1% ($325) of their annual income towards a benchmark plan. If the enhanced tax credits expire, this same individual would pay nearly 6% of their income ($1,562 annually) towards a benchmark plan in 2026. In other words, if the enhanced tax credits expire, this individual would experience an increase of $1,238 in their annual premium payments net of the tax credit.

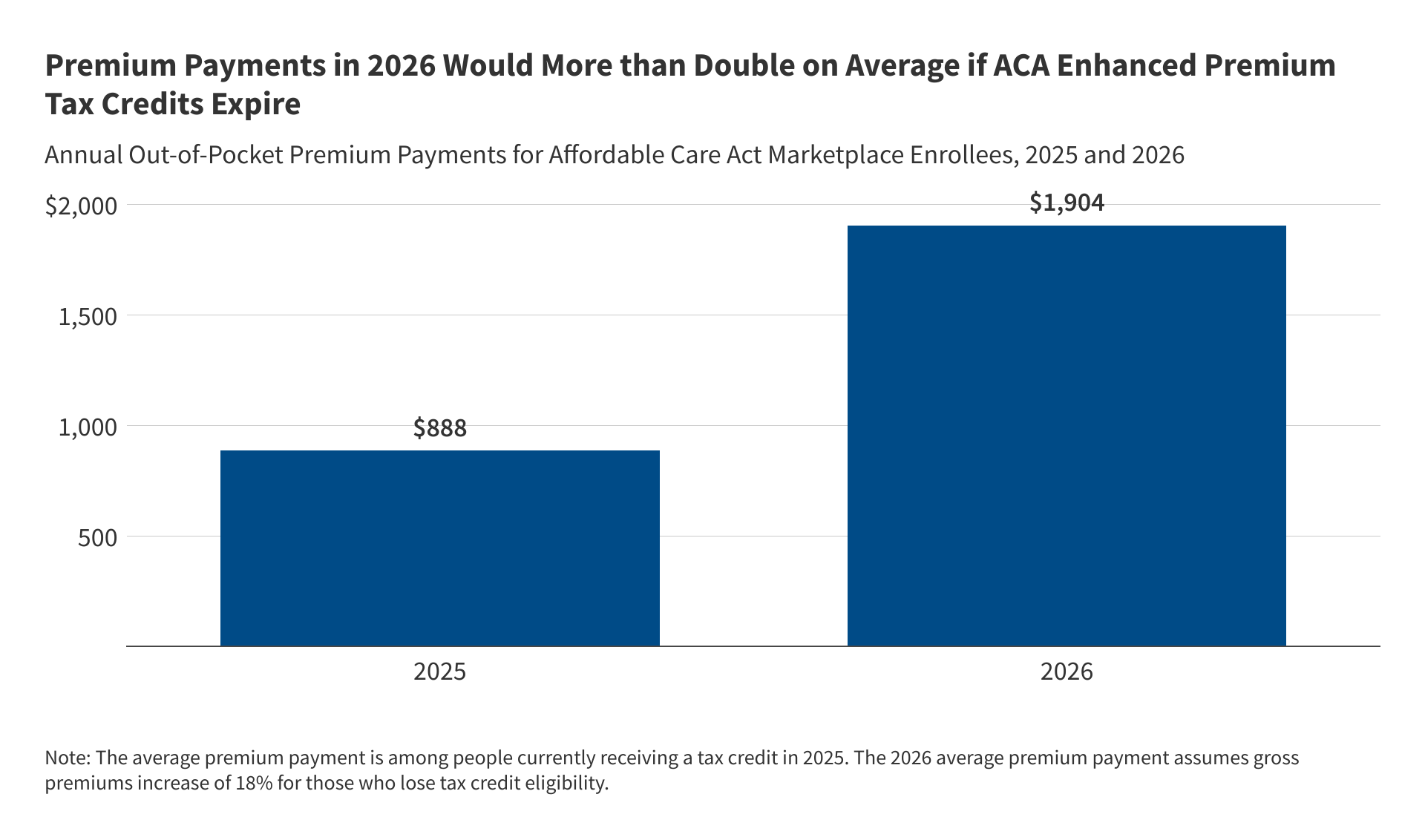

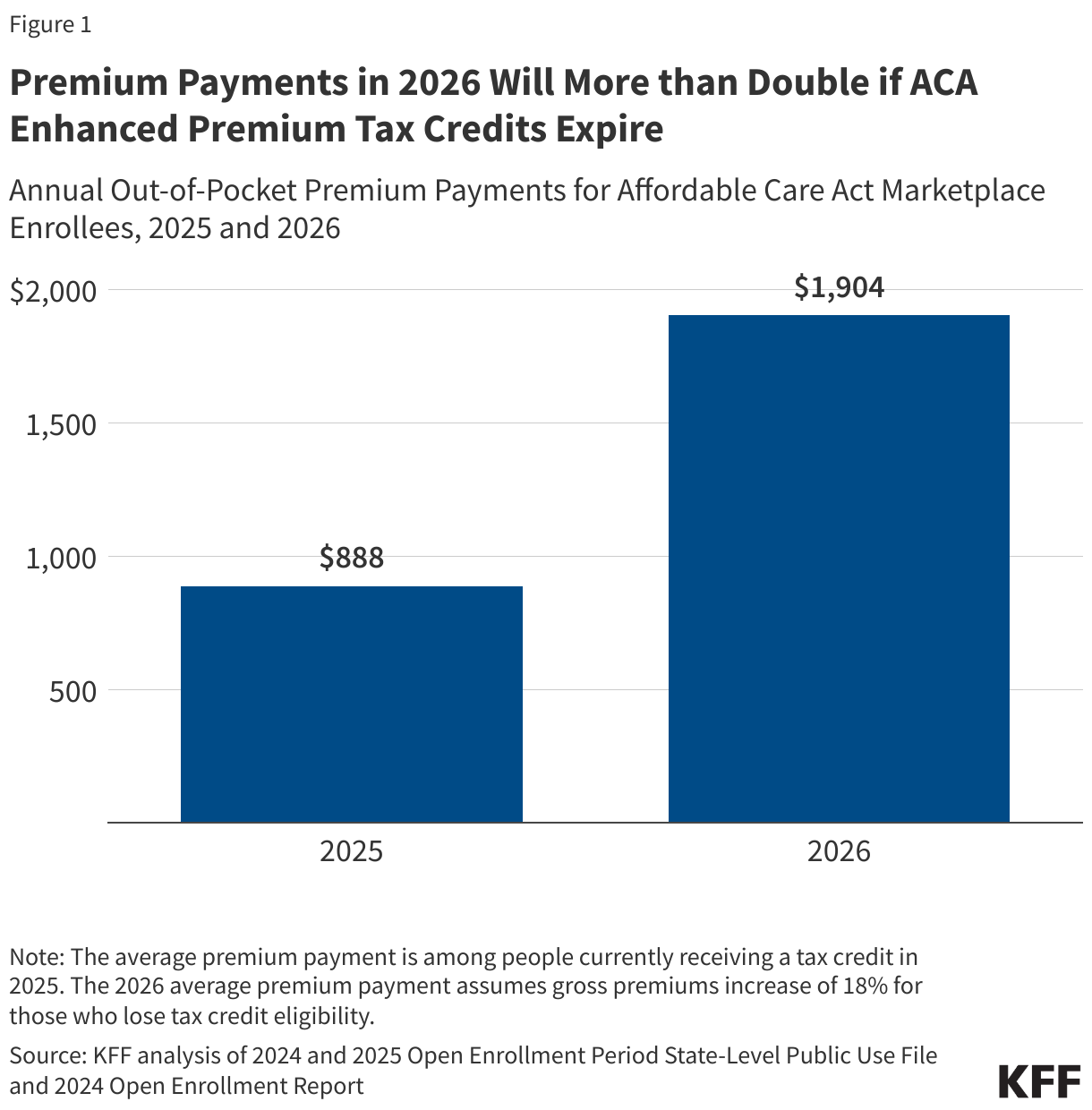

A previous KFF analysis, based on data released by the federal government, showed the enhanced premium tax credits saved subsidized enrollees an average of $705 annually in 2024, bringing their annual premium payment down to $888. Without the enhanced premium tax credits, annual premium payments in 2024 would have averaged $1,593 (over 75% higher than the actual $888). More recent data have not been released.

Based on the earlier federal data and more recent other publicly available information, KFF now estimates that, if Congress extends enhanced premium tax credits, subsidized enrollees would save $1,016 in premium payments over the year in 2026 on average. In other words, expiration of the enhanced premium tax credits is estimated to more than double what subsidized enrollees currently pay annually for premiums—a 114% increase from an average of $888 in 2025 to $1,904 in 2026. (The average premium payment net of tax credits among subsidized enrollees held steady at $888 annually in 2024 and 2025 due to the enhanced premium tax credits).

The increase in premium payments with expiration of the enhanced premium tax credits is even higher than previously estimated for two reasons:

- Trump administration changes to tax credit calculations, and

- Rising 2026 premiums.

The Trump administration made changes to the way tax credits are calculated, which were finalized in the ACA Marketplace Integrity and Affordability rule. The required contribution levels that will be in place for 2026 if the enhanced tax credits are not renewed will be higher relative to the required contribution levels calculated under the original methodology based on rules in effect at the time. This means that enrollees are expected to pay a higher share of their income towards a benchmark premium plan in 2026 than they otherwise would have.

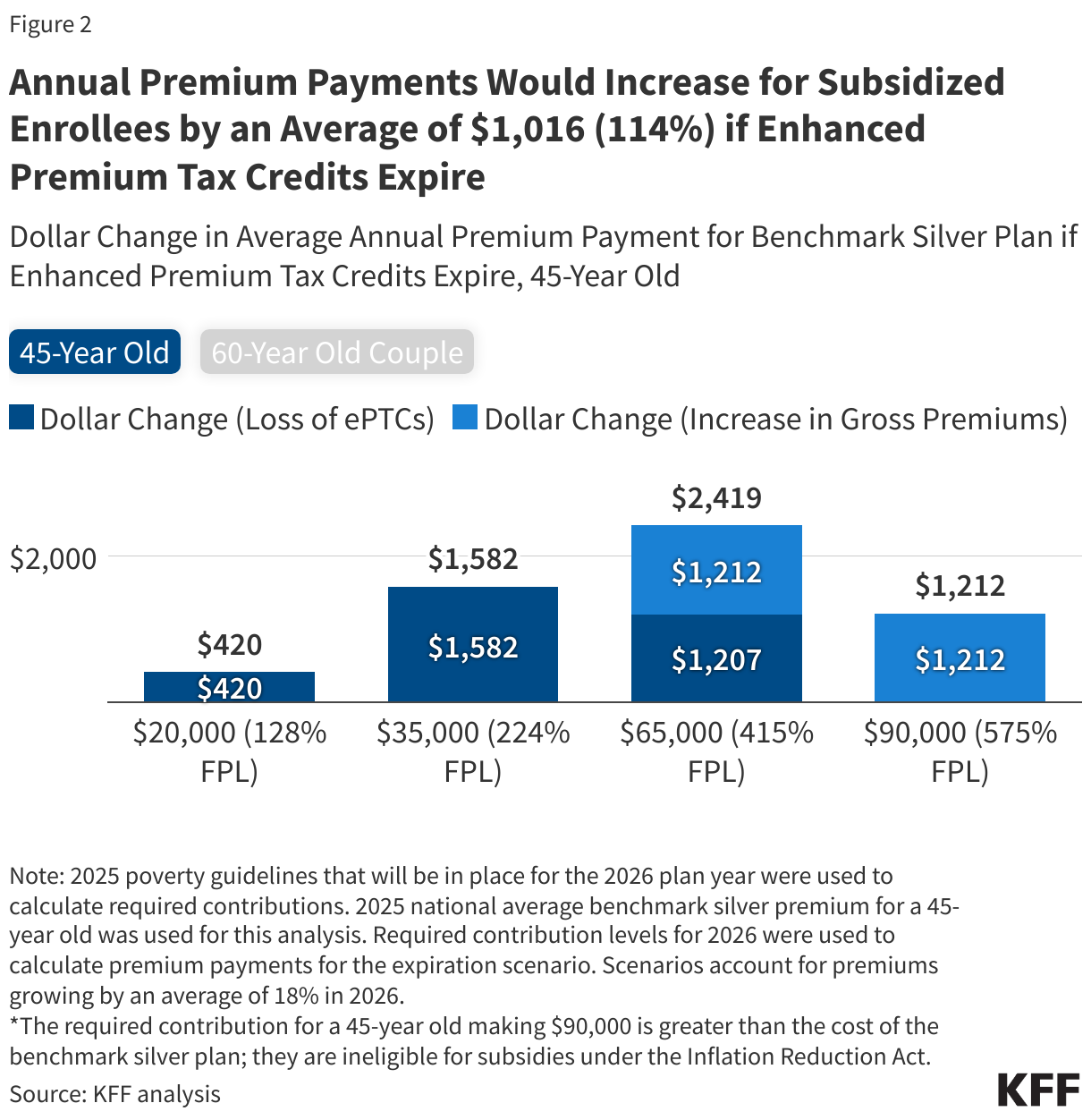

Additionally, insurers in the ACA Marketplace are proposing to raise their rates by a median of 18%. Fueled by rising health care costs and the expiration of the enhanced premium tax credits, insurers are proposing the largest rate increases in 2026 since 2018, the last time uncertainty over federal policy changes contributed to sharp premium increases. As premiums increase, the enhanced tax credits provide additional savings to enrollees that receive them. This means that middle-income enrollees, whose payment for a benchmark plan is currently capped at 8.5% of their income and will lose financial assistance altogether, will have to cover the cost of premium increases in addition to the amount their tax credits would have previously covered to keep their same plan.

Enrollees across the income spectrum can expect big increases in premium payments

Enrollees with incomes above 400% of poverty will be subject to large increases in premium payments if enhanced premium tax credits expire. On average, a 60-year-old couple making $85,000 (or 402% FPL) would see yearly premium payments rise by over $22,600 in 2026, after accounting for an annual premium increase of 18%. This would bring the cost of a benchmark plan to about a quarter of this couple’s annual income, up from 8.5%. Meanwhile, a 45-year-old earning $20,000 (or 128% FPL) in a non-Medicaid expansion state would see their premium payments for a benchmark plan rise from $0 to $420 per year, on average, from the loss of enhanced premium tax credits. About half (45%) of ACA Marketplace enrollees have incomes between 100-150% of poverty, about a fourth (28%) have incomes between 150-250% of poverty, and roughly 1 in 10 have incomes above 400% of poverty.

Methods

The average savings by income group for 2024 were taken from the 2024 Open Enrollment report. The average yearly premium savings from enhanced premium tax credits (ePTC) for enrollees under 400% FPL were defined as the sum of the differences between the required contribution amounts with and without ePTC, using the estimated percent of plan selections with ePTC by income category and assuming a uniform income distribution within each category. To extrapolate to 2026, income was inflated by the ratio of the 2025 federal poverty guidelines to the 2023 federal poverty guidelines for an individual in the continental US. For each income category, the savings were assumed to grow as the ratio of the savings between 2026 and 2024. Due to a provision in the reconciliation bill related to subsidized ACA Marketplace eligibility for immigrants, no enrollees under 100% FPL are assumed to receive premium tax credits in 2026 and are thus not included in the calculation of average savings. For enrollees at or above 400% FPL, savings were defined as difference between the average unsubsidized premium and 8.5% of the average individual income, the required contribution under the enhanced tax credits for enrollees in this income category. For 2026, the average unsubsidized premium was assumed to be 18% higher than the 2025 average unsubsidized premium, based on analysis of rate filings. Calculations assume that there are no changes in plan selection, family composition, income relative to FPL, and geography between 2024 and 2026. The annual premium payment for 2026 comprises the estimated savings from enhanced tax credits in 2026 and the average premium payment among subsidized enrollees in 2025 obtained from the 2025 Open Enrollment State-Level Public Use File. State-funded subsidies might offset some increases of premiums but are not accounted for in the estimation. Numbers from the Open Enrollment report for estimated consumer APTC savings due to the ARP and IRA by income category (Table 8) were reported as whole numbers; a Monte Carlo method was used to account for this rounding, keeping all observations that rounded to the grand mean listed in the report.