Access to contraception is a key element in shaping health and well-being for many women in their reproductive years. The Affordable Care Act (ACA) created a minimum set of benefits for most health plans regulated by the federal government and states, requiring most private plans to cover, without any cost sharing, the full range of FDA-approved contraceptives and services as a preventive service. In the years since its implementation in 2012, there has been a sharp decrease in the share of privately insured women who pay out of pocket costs for their prescribed contraceptives. Despite its impact reducing costs for women, the contraceptive coverage requirement has been one of the most contentious elements of the ACA leading to heated policy debates and multiple lawsuits, including three cases that reached the Supreme Court. Since the passage of the ACA, Presidential administrations have taken divergent approaches to the regulations that affect how this provision is implemented. For example, during the first Trump administration, the Department of Health and Human Services (HHS) and other related agencies promulgated a regulation that provided a broad exception to the contraception requirement to employers or plan with religious or moral objections to contraception. The Biden administration issued a proposed regulation, that was ultimately withdrawn, that would have expanded contraceptive coverage to include over-the-counter methods.

It is not known what, if any, actions the current Trump administration will make regarding contraceptive coverage. With major plans for reorganization of agencies within HHS including HRSA, the agency that has issued the contraceptive coverage requirement under the ACA rules, as well as actions to dismantle and restructure federal advisory committees, the future of contraceptive coverage is not clear. Concern about the future of this provision has spurred multiple efforts by Congressional Democrats and some state legislatures to enshrine the right to contraception, especially since Roe v Wade was overturned by the Supreme Court. This issue brief explains the rules for private insurance coverage of contraceptives at the federal and state level, the exemptions and accommodations available for certain employers, gaps in coverage for contraceptives obtained outside of the traditional clinical setting, and how changes in the agencies responsible for making contraceptive recommendations may affect coverage for contraceptives.

Use of Contraception

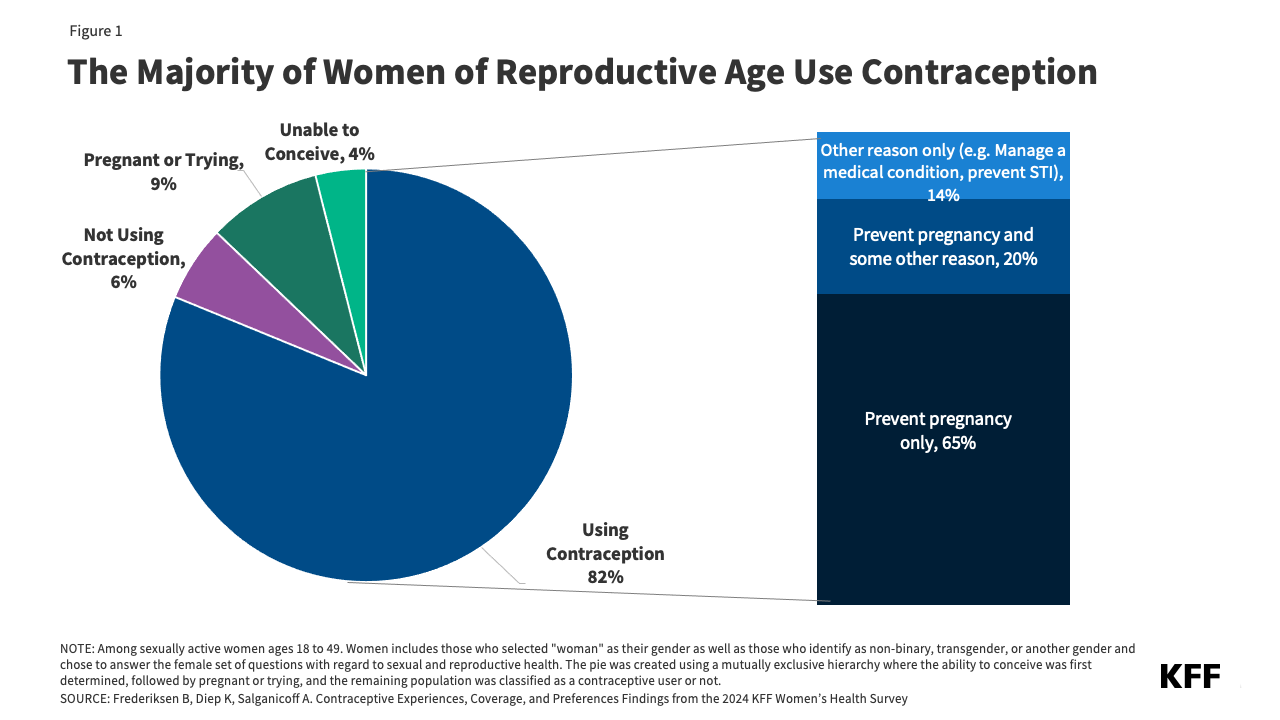

Contraceptive care is an important component of overall health care for many people in their reproductive years, and most women use contraception at some point in their lifetime. The majority (82%) of women of reproductive age (18 to 49) say they used some form of contraception in the past 12 months (Figure 1) and three quarters say that preventing a pregnancy is very or somewhat important to them. While most women who use contraception use it to prevent pregnancy (65%), one in five (20%) use it to both prevent pregnancy and for some other reason (such as managing a medical condition or preventing a sexually transmitted infection) and 14% use it solely for reasons outside of preventing pregnancy (such as to regulate their periods or manage acne). Among women who use contraception, nearly half (48%) report using more than one kind of contraceptive method in the past 12 months. Three in 10 (31%) women rely on permanent methods (either their own sterilization or their partner’s) and one in four (24%) used long-acting reversible methods (LARCS) like intrauterine devices (IUDs) or contraceptive implants. Four in ten (40%) women use short acting hormonal methods, with three in 10 (29%) relying on oral contraceptive pills.

Despite the fact that the ACA has been in place for 15 years, there are still gaps in awareness that federal law requires most private plans to cover the full cost of contraceptives. Among women of reproductive age, less than half (43%) know that plans are required to cover all FDA approved prescribed contraceptives. Higher shares of Black women are aware of this requirement compared to White women (49% vs. 42%). Notably, less than half (44%) of women with private insurance coverage, for whom this requirement applies, are aware that most insurance plans are required to pay the full cost of birth control for women.

ACA Federal Requirements for Contraceptive Coverage and State Laws

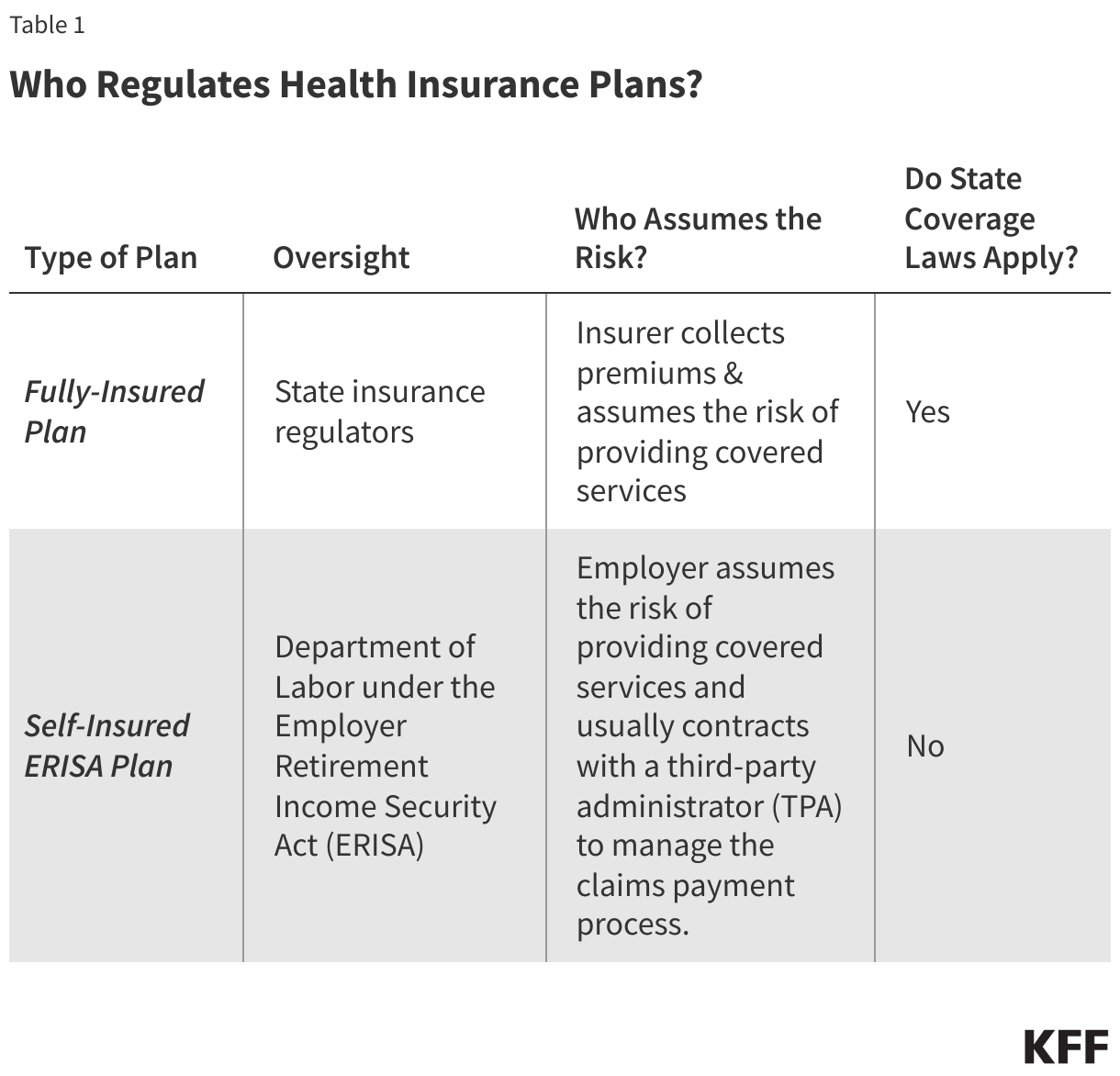

The Affordable Care Act requires most private plans to cover a range of recommended preventive health services provided by in-network health care providers, including contraceptives, without any cost-sharing (such as copays, deductibles or co-insurance). This requirement applies to all private plans—fully insured and self-insured plans in the individual, small group, and large group markets, except those that maintain “grandfathered” status. Individual, small, and large group plans are regulated by the state, whereas self-insured plans are regulated by the federal government under the Employee Retirement Income Security Act (ERISA). The required preventive health services for adults are those that: receive an A or B recommendation by the U.S. Preventive Services Task Force (USPSTF); are recommended by the Health Resources and Services Administration (HRSA) currently based on guidelines issued by the Women’s Preventive Services Initiative (WPSI), the expert body currently commissioned by HRSA to issue and update preventive clinical recommendations for women; and vaccine recommendations for children and adults made by the Advisory Committee on Immunization Practices (ACIP).

The HRSA contraceptive services and counseling recommendation requires plans to cover all FDA-approved, -granted, or -cleared contraceptive methods, as well as sterilization procedures, and patient screening, education, and counseling for all adolescent and adult women. This also includes any follow-up care that is required, as well as insertion and removal of implants and IUDs. The initial 2011 HRSA recommendation included the language “as prescribed” in reference to the coverage requirement for contraception. When WPSI updated the contraceptive coverage recommendation in 2021, it did not include a prescription requirement for coverage of contraception. HRSA subsequently dropped the prescription requirement in its language when the preventive services guidelines were updated and posted. While “as prescribed” is only referenced in the U.S. Departments of Labor, Health and Human Services, and Treasury (“tri-agency”) federal FAQs, plans are “encouraged” but are not required to cover over-the-counter methods, and very few do without a prescription.

Over the years, the federal tri-agency has released additional guidance clarifying the contraceptive coverage requirement. Some of this guidance has been adopted into the updated versions of the contraceptive recommendation, such as the requirement that plans must cover without cost-sharing at least one product within each FDA -approved, granted, or cleared contraceptive method category. Federal guidance clarifications include:

- Clarifying that plans must cover any contraceptives that are deemed “medically necessary” by a health care provider for an individual, including brand name drugs if a generic is not available, a clinician-recommended brand name product, and contraceptive products that are not specifically identified by HRSA, such as new contraceptive products approved by the FDA.

- Requiring plans to have an exceptions process in place for individuals whose health care provider has determined that a different contraceptive within a category (including a brand name or a different generic), that is not the one covered without cost-sharing by the plan, is “medically appropriate” for them. The exceptions process must be easily accessible and timely for patients and providers to request coverage for a medically necessary contraceptive.

- As an alternative to covering one method within each contraceptive category without cost-sharing, plans can also choose to cover all products within a contraceptive category that have no therapeutic equivalents (with the same active ingredients, dosage form, route of administration, and strength). For example, plans could choose to cover all types of hormonal IUDs currently available in the US, since none of them has a therapeutic equivalent.

Plans can use reasonable medical management to control costs and promote efficient delivery of contraceptive care. Within the categories of contraceptives that must be covered, plans may limit coverage in these categories to generic drugs and can impose cost-sharing for equivalent branded drugs. However, as noted above, plans must cover with no cost-sharing any brand names or therapeutically equivalent products that a health provider deems as “medically appropriate” for an individual. Federal guidance has also clarified that plans are not allowed to require individuals to first fail using some methods (like oral contraceptive pills) before covering a different method (such as IUDs) and cannot require that individuals first fail using certain products within a category (e.g. requiring a person to first fail using pill A before covering pill B). Plans cannot impose age limits to contraceptive services, since the recommendation applies to women with reproductive capacity.

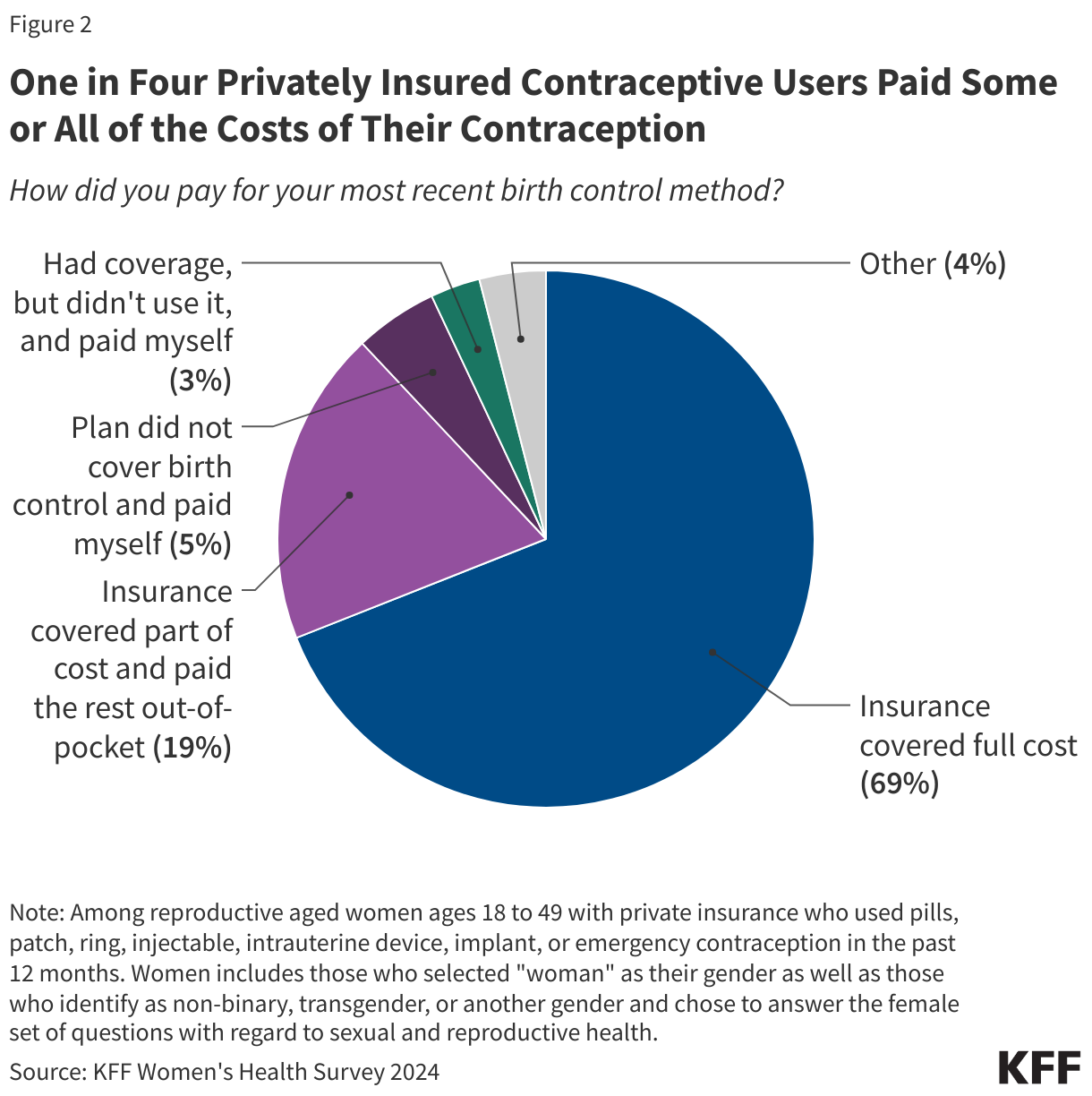

Since the implementation of the ACA’s contraceptive coverage provision, fewer women are paying out of pocket for contraceptives. Research has found that the share of women with employer sponsored coverage who pay $0 for oral contraceptives, injectables, vaginal rings and IUDs has dramatically increased since the contraceptive coverage requirement took effect. However, a significant share of privately insured women are still paying out of pocket. Among privately insured contraceptive users, one in four (24%) report paying out-of-pocket for some or all of their contraception because their plan did not cover the full cost (Figure 2). Reasons for having out-of-pocket costs could include being enrolled in a grandfathered plan, working for an employer that has a religious objection to covering contraception, going to an out of network provider, or using a brand name method that has a generic alternative.

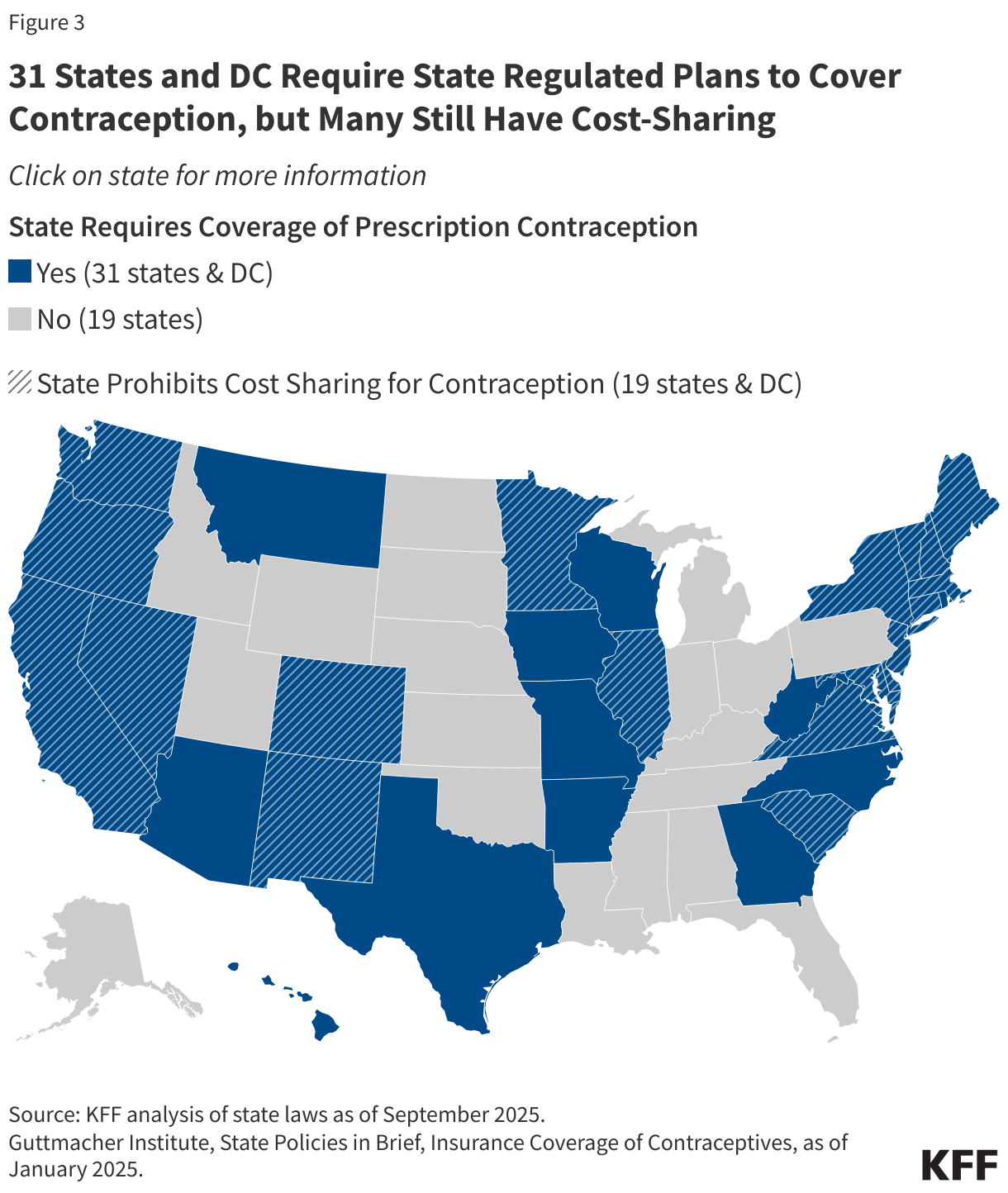

Before the ACA, coverage for prescription contraceptives was generally widespread in the private and public sectors, but not universal, and typically subject to cost-sharing. Unless a state had a contraceptive coverage mandate, insurers and employers could choose whether or not to provide coverage for contraception. In 2000, a ruling by the Employment Equal Opportunity Commission found that employers that covered preventive prescription drugs and services, but did not cover prescription contraceptives were in violation of the Civil Rights Act. Currently, 31 states and DC have laws requiring insurance plans to cover contraceptives and 19 states and DC prohibit cost sharing (Figure 3). State laws, however, fall short of universal coverage. They only apply to state regulated plans (Table 1), but not self-funded plans where 67% of covered workers are insured and many of these state laws also do not require plans to cover the full range of contraceptive products or do not prohibit cost-sharing (Appendix Table 1). If the ACA preventive services requirement were invalidated by the courts, only individuals with fully-insured state plans living in states with laws requiring contraceptive coverage would be guaranteed some sort of coverage.

Exemptions and Accommodations to the Contraceptive Coverage Requirement

While most employers are required to include contraceptive coverage in their plans, houses of worship can choose to be exempt from the requirement if they have religious objections. This exception means that women workers and female dependents of exempt employers do not have guaranteed coverage for either some or all FDA -approved, -granted, or -cleared contraceptive methods if their employer has an objection. Meanwhile, religiously- affiliated nonprofits and closely held for-profit corporations are not eligible for an exemption but can choose an accommodation (Figure 4). This option was first offered to religiously-affiliated nonprofit employers and then extended to closely held for-profits after the Supreme Court ruling in Burwell v. Hobby Lobby. The accommodation allows these employers to opt out of providing and paying for contraceptive coverage in their plans by either notifying their insurer, third party administrator (TPA), or the federal government of their objection. The insurers are then responsible for covering the costs of contraception, which assures that their workers and dependents have contraceptive coverage while relieving the employers of the requirement to pay for it. Because the federal government does not track this information, it is not known how many employers or plans do not cover or only provide partial coverage for contraceptive services and supplies.

Despite its far-reaching impact, the ACA’s requirement for contraceptive coverage has been challenged in the courts on multiple occasions, with three cases reaching the Supreme Court. The earlier cases, Burwell v. Hobby Lobby (2014) and Zubik v. Burwell (2016), challenged the Obama Administration’s regulations implementing the contraceptive coverage requirement, contending that the requirement violated some employers’ religious rights. The most recent cases, Little Sisters of the Poor v. Pennsylvania (2020) and Trump v. Pennsylvania (2020), involved regulations issued by the first Trump Administration in 2018. These regulations allowed any nonprofit or for-profit employers, including private institutions of higher education, with religious objections to contraception coverage and all but publicly-traded employers with moral objections to qualify for an exemption and exclude contraceptive coverage from their plans.

In August 2025, a U.S. District Court issued a ruling in Commonwealth of Pennsylvania v. Trump in favor of Pennsylvania vacating the 2018 Trump regulations. The court found the regulations are arbitrary and capricious and were promulgated in excess of Defendants’ statutory authority and in violation of the Administrative Procedure Act’s (“APA”). The Trump administration has appealed this ruling to the Third Circuit Court of Appeals. While the Obama regulations allowing only houses of worship to be exempt are now in effect, it is not clear whether employers that dropped some or all contraceptive coverage under the Trump regulations are now in compliance or whether the Trump administration will enforce these regulations while the litigation proceeds.

Gaps in Coverage for Contraceptives Outside of the Traditional Clinical Setting

Over the past 15 years there have been efforts to broaden contraceptive availability outside of traditional clinical settings, including through commercial apps that use telehealth platforms, state efforts to allow pharmacists to prescribe birth control, and, most recently, over-the-counter (OTC) access to contraceptives without a traditional prescription. However, because the ACA’s contraceptive requirement only applies to contraception prescribed by in-network health care providers as well as challenges working getting insurance providers to work with non-traditional venues, it has been nearly impossible for individuals to obtain contraception at no cost from these new avenues using their insurance or Medicaid.

Telecontraception: A variety of online platforms are providing a new option for people to conveniently obtain contraceptive supplies that need a prescription without the need for an in-person visit (“telecontraception”). While these platforms offer a variety of brands and generic equivalents, and most offer a $10 to $15 per month oral contraception option, many report barriers working with private insurance companies. Companies that accept insurance have reported that private insurance companies are sometimes unwilling to cover contraceptive mail order deliveries beyond the first few months, likely due to pharmacy contract limitations and competition by the private insurance companies’ internal mail orders. Companies have also experienced issues with Pharmacy Benefit Managers (PBM) placing limits on refills from the telecontraception company and requiring patients to use their insurance companies PBM mail order program. One company also reported that they are considered an out-of-network provider, which means that their clients can be charged copays.

Over-the-Counter Contraceptives: In July 2023, the FDA approved the progestin-only Opill for over the counter (OTC) use, making it the first OTC daily oral contraceptive pill available for over-the-counter purchase in the U.S. without age restriction in stores and online. The suggested retail price of Opill is $19.99 for one month’s supply or $49.99 for a three-month supply. While the ACA currently requires most private plans to cover contraceptives without cost-sharing, as discussed earlier, plans typically require a prescription to trigger coverage, even for contraceptive methods that are available OTC without a prescription (such as emergency contraception). Currently, eight states (CA, CO, DE, MD, NJ, NM, NY, and WA) have laws or regulations requiring state-regulated private health insurance plans to cover, without cost sharing, some or all OTC contraception without a prescription. Requiring all plans to cover non-prescribed contraceptives would require legislation at the federal level or administrative changes to the ACA’s preventive services policy. Federal FAQs from July 2022 encourage, but do not require, plans to cover without cost sharing OTC emergency contraceptive products that are purchased without a prescription. In October 2024, the Biden Administration proposed a new rule that would have required most private plans to cover OTC methods purchased without a prescription from an in-network pharmacy and would have required plans to disclose to enrollees that OTC products were included in their coverage. In January 2025, days before the end of their presidential term, the Biden administration withdrew the proposed regulation.

Pharmacist Prescribing: Thirty-five states and D.C. have passed laws to allow pharmacists to prescribe certain self-administered contraceptives to women, such as oral contraceptives, emergency contraception, the patch and the vaginal ring. In these states pharmacist prescribing helps reduce barriers to accessing contraception by removing the need to visit a clinician to obtain a prescription, and for people without insurance, it can be less expensive than getting a prescription from a clinician. However, challenges remain for women seeking a prescription for contraception from a pharmacist. For example, pharmacies typically charge consultation fees, which some reports suggest can be as high as $50 in certain areas. While insurers are generally required to cover contraceptives without cost sharing, they are not obligated to cover this fee. This lack of payment can lead to pharmacies charging patients a consultation fee.

The Future of Contraceptive Coverage

Changes in the Department of HHS and the agencies responsible for making women’s preventive health services recommendations may affect access and coverage to contraceptives. HHS under the Trump Administration has announced a proposal that would make major changes go through a “transformation to Make American Healthy Again.” Should this proposal be implemented, they could result in elimination of many positions and significant restructuring and consolidation of the divisions within HHS. HRSA, along with the Office of the Assistant Secretary for Health (OASH), the Substance Abuse and Mental Health Services Administration (SAMHSA), the Agency for Toxic Substances and Disease Registry (ATSDR), and the National Institute for Occupational Safety and Health (NIOSH) would be combined to form a new division, the Administration for a Health America (AHA). The statutory language in the ACA specifically names HRSA as the division responsible for making preventive services recommendations for women and it is unclear how or whether this new consolidated agency would be able to make updates or make new recommendations given the specificity of HRSA as the agency responsible for issuing the coverage guidelines for women’s preventive services in section governing coverage of preventive services in the ACA law.

The American College of Obstetricians and Gynecologists (ACOG), the organization that convenes the WPSI panel of leading medical and health professional organizations that make recommendations to for women’s preventive services to HRSA, has publicly announced that it will stop accepting federal funds for any continuation of its current contracts following changes in federal funding guidelines by the Trump administration, citing that “Recent changes in federal funding laws and regulations significantly impact ACOG’s program goals, policy positions, and ability to provide timely and evidence-based guidance and recommendations for care.” In their letter, ACOG has stated that they will continue the work, but the decision to withdraw was applauded by a Trump administration spokesman. Prior to this announcement, Project 2025 and other anti-abortion advocates had called for the federal government to cut ties with ACOG. It is not clear how the Trump Administration will proceed after the ACOG contract expires. Whether HRSA or a new AHA agency would contract with a different organization or convene its own panel is unknown. HHS could convene a new panel to make new contraceptive recommendations or make changes to the existing one. Project 2025 and other anti-abortion organizations have called for removing IUDs and the emergency contraception pill Ella from the contraceptive coverage requirement, based on the false claim they prevent the implantation of a fertilized embryo. Research has consistently found that emergency contraception pills do not terminate a pregnancy, stop the implantation of a fertilized egg, nor affect a developing embryo and is stated on the product information available on the FDA website.

In addition, the courts continue to litigate different aspects of the ongoing preventive health services case Braidwood v. Kennedy. A federal district court is currently considering whether the Secretary of Health and Human Services’ ratification of HRSA and ACIP recommendations violates the Administrative Procedure Act and thus invalidates the preventive services issued by these agencies, including contraceptive coverage. In the original case, filed in 2022, the respondents claimed that the preventive services requirements for private health insurance are unconstitutional and that the requirement to cover pre-exposure prophylaxis treatment (PrEP) (medication to prevent getting HIV from sex or injection drug use for those at risk) violates the Religious Freedom Restoration Act (RFRA). The Supreme Court ruled in June 2025 that the ACA requirement that most private insurers and Medicaid expansion programs cover preventive services recommended by USPSTFwith no cost-sharing is constitutional. Depending on how the District Court rules regarding HRSA and ACIP and whether there are appeals to the ruling, this case may end up before the Supreme Court once again.