Medicare Advantage plans, which enrolled more than 34 million Medicare beneficiaries or 54% of the eligible Medicare population in 2025, typically offer extra benefits, such as dental, vision, and hearing, often for no additional premium, as well as lower cost sharing compared to traditional Medicare without supplemental insurance. These additional benefits usually come with the trade-off of more restrictive provider networks and greater use of cost management tools, such as prior authorization.

This brief provides an overview of premiums and benefits in Medicare Advantage plans that are available for 2026 and key trends over time. This brief uses data from the CMS Landscape and Benefit files. See methods for more details. In general, this brief refers to individual Medicare plans available for general enrollment, which excludes Special Needs Plans (SNPs), except where noted, and excludes employer plans. A companion analysis describes trends in plan offerings.

Medicare Advantage Highlights for 2026

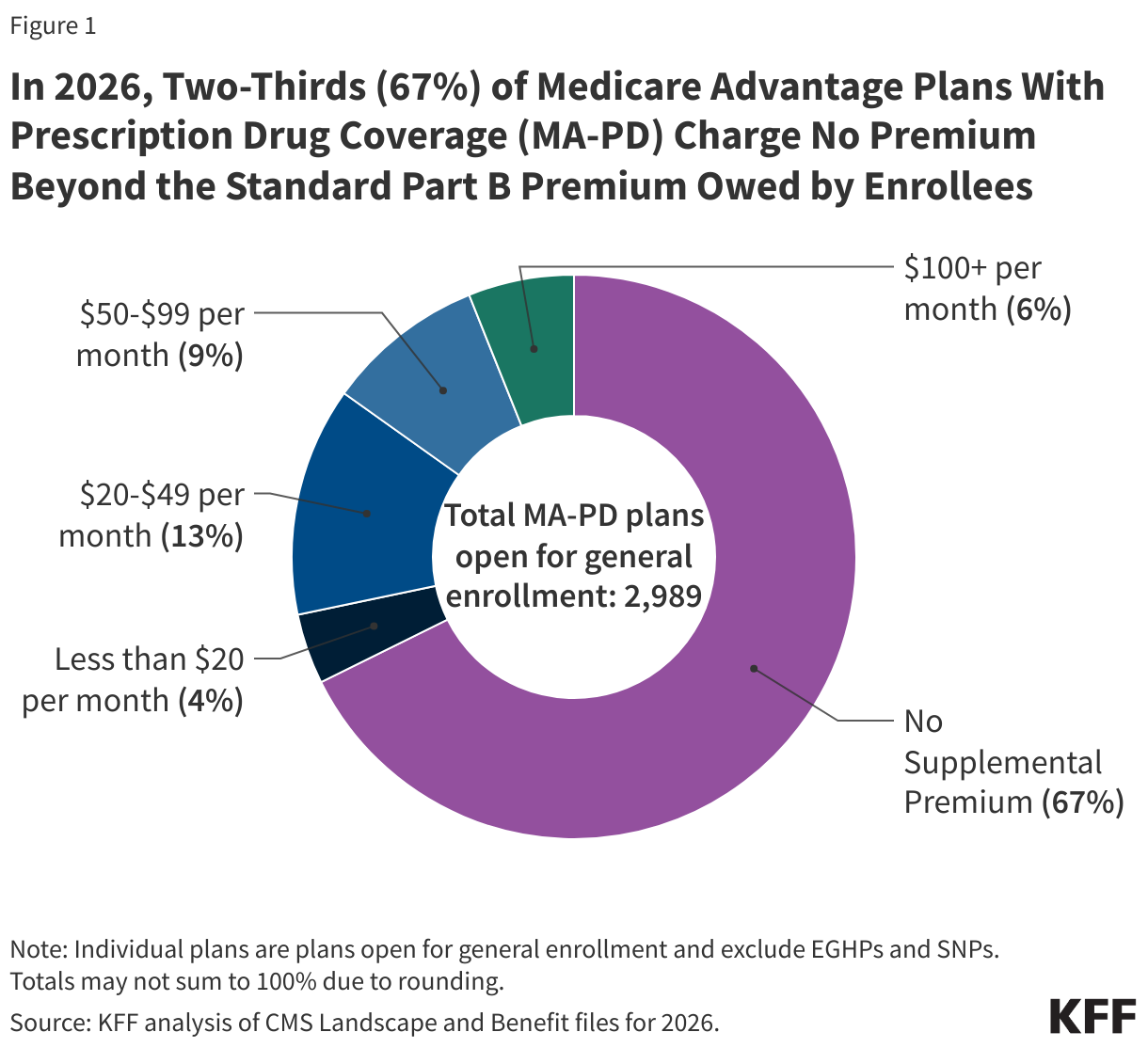

- Two-thirds of all Medicare Advantage plans with Part D prescription drug coverage (MA-PDs) (67%) will charge no premium (other than the Medicare Part B premium) in 2026, the same as 2025.

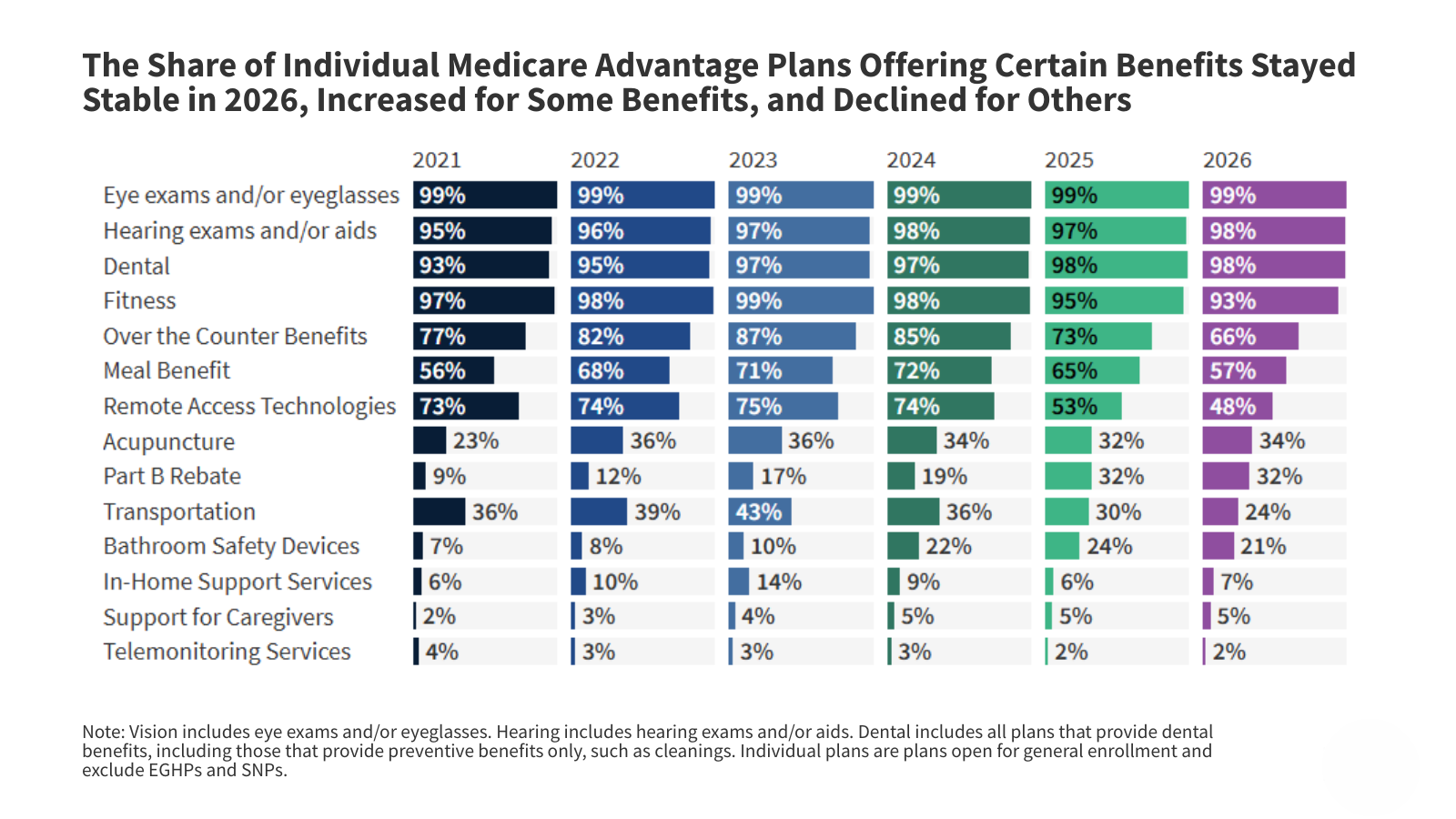

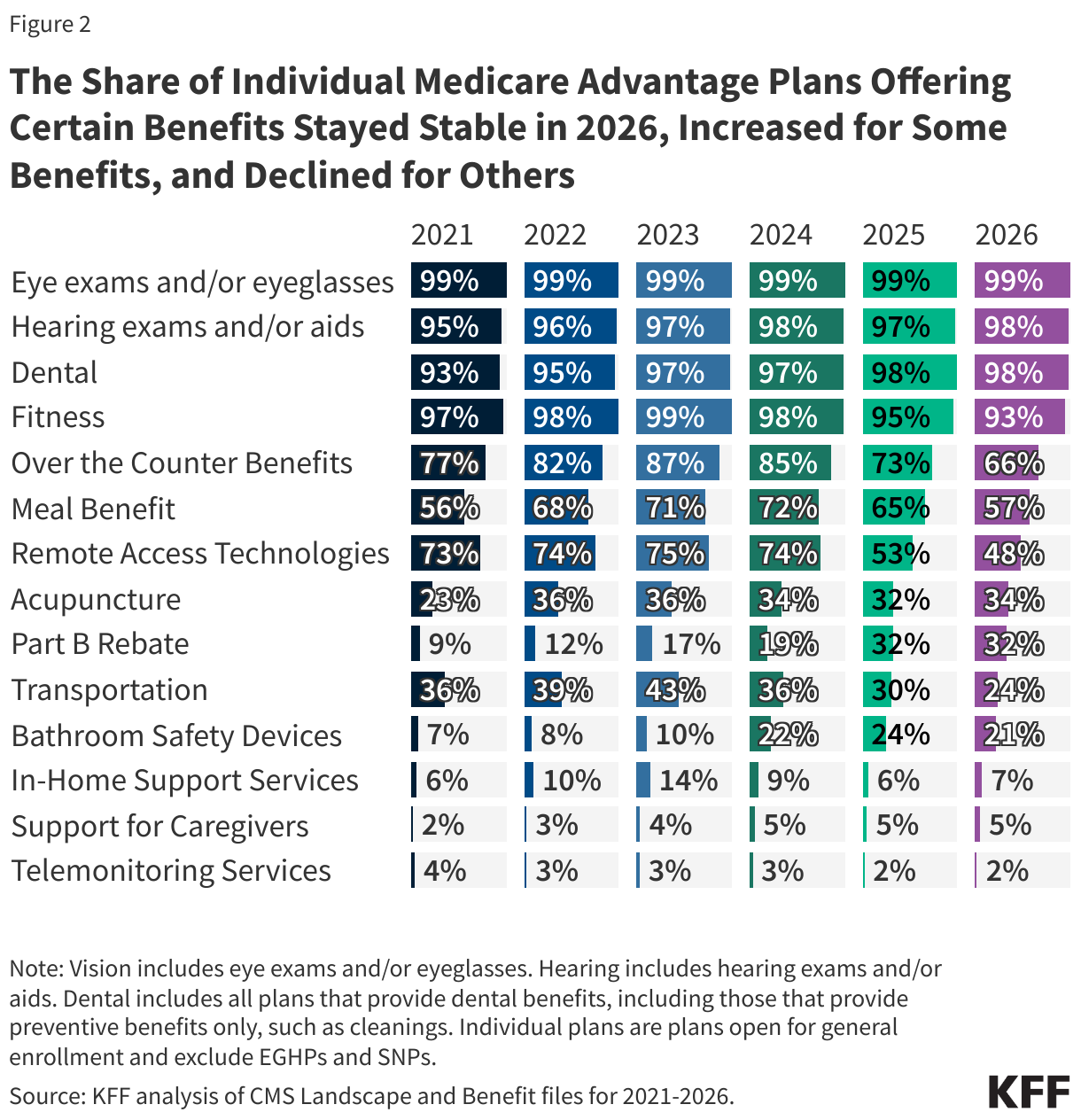

- While nearly all individual Medicare Advantage plans (98% or more) are offering vision, dental and hearing benefits, as they have in previous years, the share offering certain other supplemental benefits has declined, such as an allowance for over-the-counter items (66% in 2026 vs. 73% in 2025), a meal benefit (57% in 2026 vs. 65% in 2025), remote access technologies (48% in 2026 vs. 53% in 2025), and transportation (24% in 2026 vs. 30% in 2025).

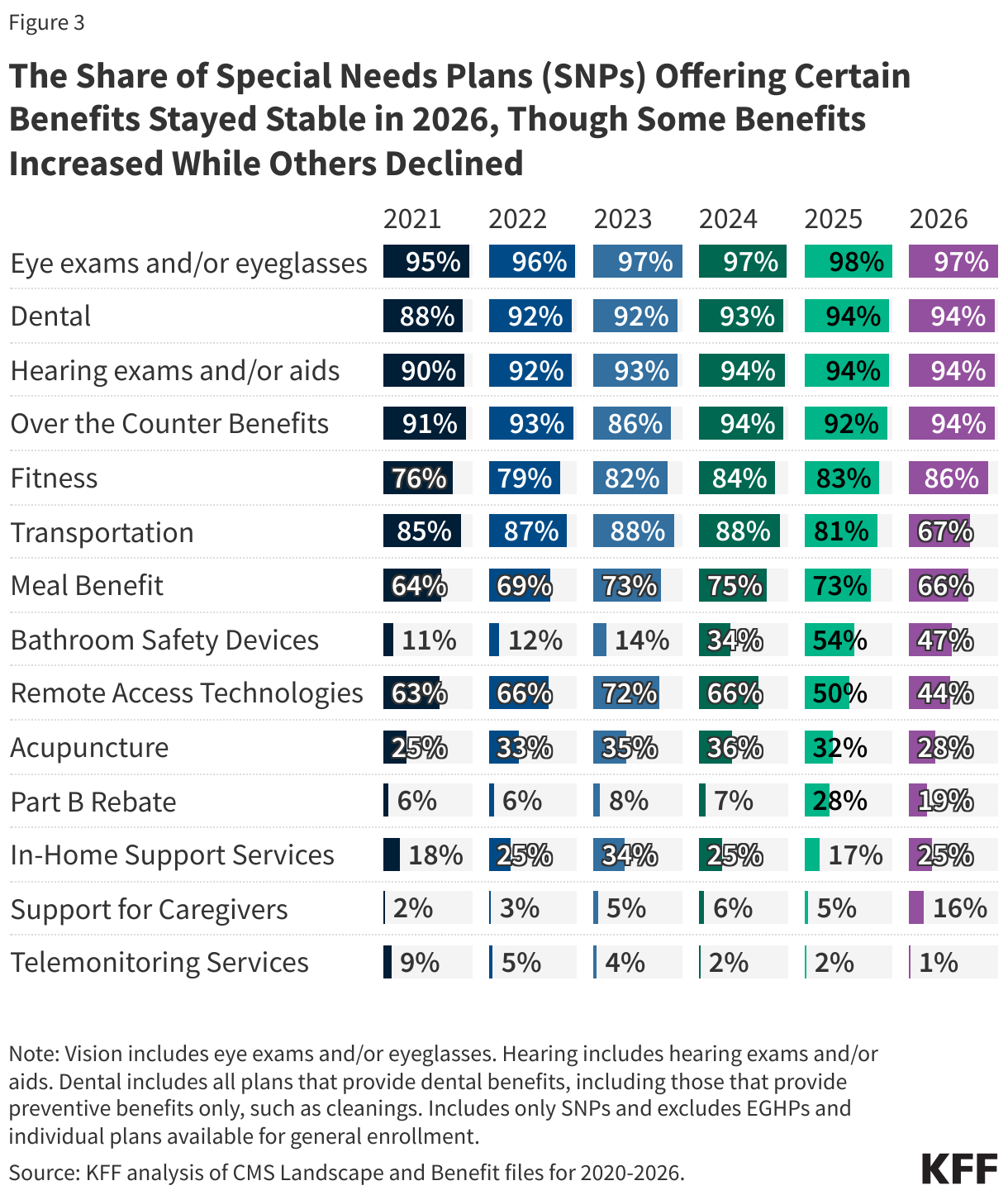

- The share of Special Needs Plans (SNPs) offering certain supplemental benefits has also declined, such as transportation (67% in 2026 vs 81% in 2025), a meal benefit (66% in 2026 vs 73% in 2025), bathroom safety devices (47% in 2026 vs 54% in 2025), and remote access technologies (44% in 2026 vs 50% in 2025), while the share offering in-home support services (25% in 2026 vs 17% in 2025) and support for caregivers (16% in 2026 vs 5% in 2025) has increased.

- In 2026, a larger share of SNPs than Medicare Advantage plans for individual enrollment offer transportation benefits for medical needs (67% for SNPs vs 24% for individual plans), an allowance for over-the-counter items (94% vs 66%), bathroom safety devices (47% vs 21%), in-home support services (25% vs 7%), and caregiver support (16% vs 5%). A smaller share of SNPs than individual plans offer acupuncture (28% vs 34%) and fitness benefits (86% vs 93%).

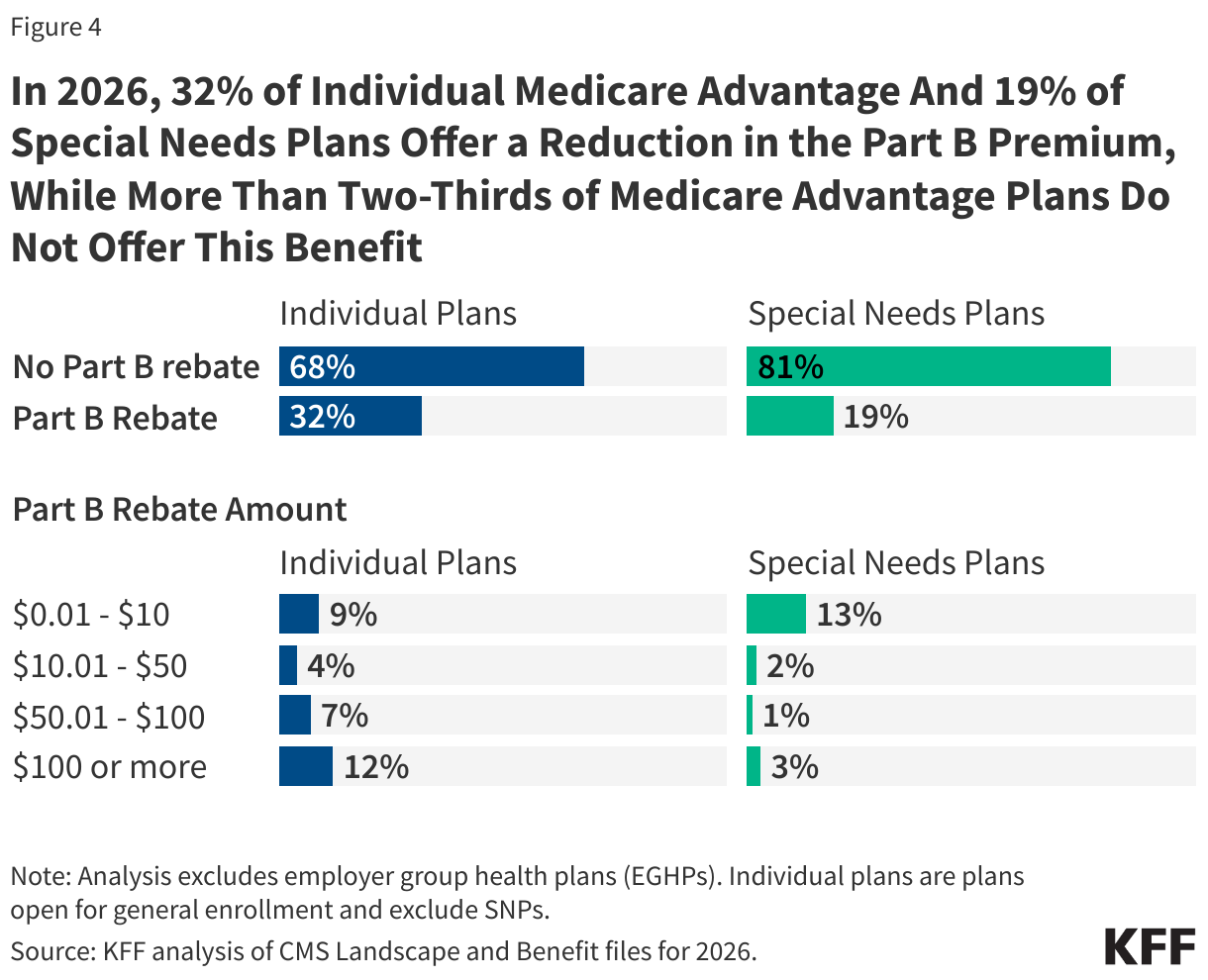

- Nearly one-third (32%) of individual Medicare Advantage plans will offer some reduction in the Medicare Part B premium in 2026 as a supplemental benefit, the same as in 2025. Among plans offering a reduction in the Part B premium, more than a third (36%) are offering a reduction of more than $100 a month, while 28% of plans are offering a reduction of $10 or less per month.

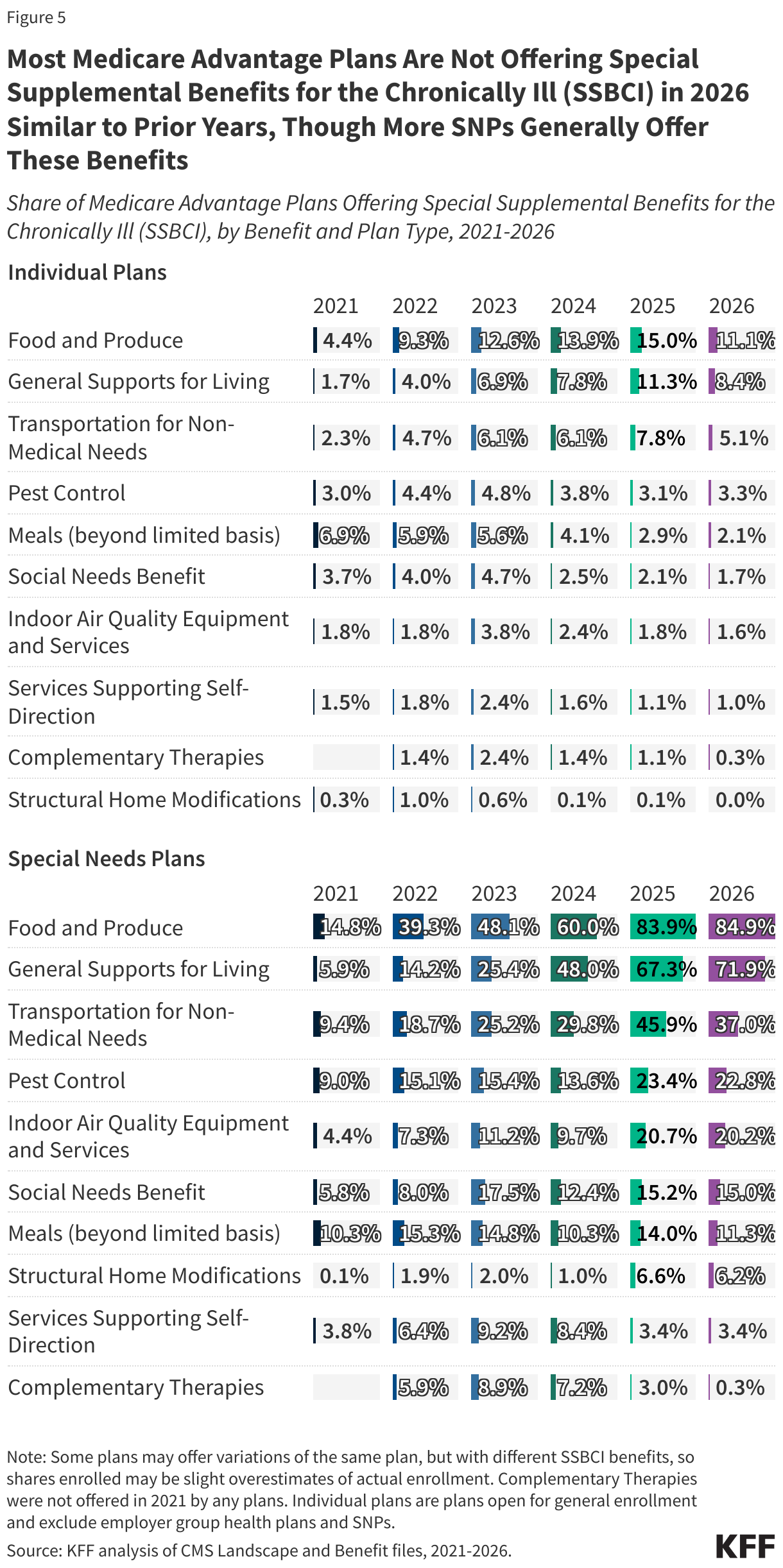

- A larger share of SNPs than other Medicare Advantage plans are offering Special Supplemental Benefits for the Chronically Ill, which are extra benefits available to a subset of a plan’s enrollees, particularly food and produce (85% in SNPs vs 11% in individual plans) and general supports for living, such as housing and utilities (72% in SNPs vs 8% in individual plans).

Premiums

The vast majority of Medicare Advantage plans for individual enrollment (89%) will include prescription drug coverage (MA-PDs), similar to 2025 (88%), and the share of MA-PDs where enrollees are responsible for the Medicare Part B premium ($202.90 per month) but no additional premium is 67% in 2026, the same as in 2025 (Figure 1). Nearly all Medicare beneficiaries (98%) have access to a MA-PD with no additional monthly premium in 2026, similar to 2025 (99%).

In 2025, more than three-quarters (76%) of enrollees in MA-PD plans pay no premium other than the Medicare Part B premium. Based on enrollment in March 2025, 9% of enrollees pay at least $50 a month, including 3% who pay $100 or more. CMS estimates that the average monthly plan premium among all Medicare Advantage enrollees in 2026, including those who pay no premium for their Medicare Advantage plan, will be $14.00 a month.

While many employers and unions also offer Medicare Advantage plans to their retirees, complete information about these 2026 plan benefits is not made available. Employer and union plans are administered separately and may have enrollment periods that do not align with the Medicare open enrollment period.

Medicare Advantage plans may offer extra benefits that are not available in traditional Medicare and are considered “primarily health related.” Plans are required by law to use rebate dollars (which may be higher for plans that qualify for the quality bonus program) to help cover the cost of extra benefits, reduce cost sharing, or reduce the Part B and/or Part D premium. Beginning in 2019, CMS expanded the definition of “primarily health related” to allow Medicare Advantage plans to offer additional supplemental benefits. Medicare Advantage plans may also restrict the availability of these extra benefits to certain subgroups of beneficiaries, such as those with diabetes or congestive heart failure, making different benefits available to different enrollees.

In 2026, 98% or more individual plans offer some vision (99%), dental (98%) or hearing benefits (98%), similar to 2025 (97% or more) (Figure 2). Though these benefits are widely available, the scope of coverage for these services varies. For example, a dental benefit may include cleanings and preventive care or more comprehensive coverage, and often is subject to an annual dollar cap on the amount covered by the plan. From year to year, plans may change the parameters of this coverage, such as increasing or decreasing annual maximums the plan will pay toward the benefit or adjusting cost sharing for services. There is not yet data available about utilization of these benefits or associated costs, so it is not clear the extent to which supplemental benefits are used by enrollees.

Some benefits are being offered by a smaller share of plans in 2026 than in 2025. For example, 66% of plans are offering an allowance for over-the-counter items (vs. 73% in 2025), while 57% are offering a meal benefit (vs. 65% in 2025), and 24% are offering transportation benefits for medical needs (vs. 30% in 2025). A similar share of plans is offering fitness benefits, acupuncture, bathroom safety devices, in-home support services, and support for caregivers of enrollees in 2026 compared with 2025 (Figure 2). This is not an exhaustive list of extra benefits that plans offer, and plans may offer other services such as home-based palliative care, therapeutic massage, and adult day health services, among others.

As of 2020, Medicare Advantage plans have been allowed to include telehealth benefits as part of the basic benefit package – beyond what was allowed under traditional Medicare prior to the COVID-19 public health emergency – which was extended to January 2026. Therefore, these benefits are not included in the figure above because their cost is not covered by either rebates or supplemental premiums. Medicare Advantage plans may also offer supplemental telehealth benefits via remote access technologies and/or telemonitoring services, which can be used for those services that do not meet the requirements for coverage under traditional Medicare or the requirements for the telehealth benefits as part of the basic benefit package (such as the requirement of being covered by Medicare Part B when provided in-person). In 2026, 48% of plans are offering remote access technologies, a decline from 53% in 2025. The same share of plans is offering telemonitoring services (2% in 2026 and 2025).

SNPs are designed to serve a higher-need population and an increasing number of beneficiaries are enrolling in SNPs. A similar share of SNPs in 2026 compared with 2025 are offering dental, vision, hearing, fitness, an allowance for over-the-counter items, and telemonitoring services (Figure 3). However, a smaller share of SNPs is offering transportation benefits for medical needs (67% in 2026 vs 81% in 2025), a meal benefit (66% in 2026 vs 73% in 2025), bathroom safety devices (47% in 2026 vs 54% in 2025), and remote access technologies (44% in 2026 vs 50% in 2025). A larger share of SNPs is offering their enrollees in-home support services (25% in 2026 vs 17% in 2025) and support for caregivers (16% in 2026 vs 5% in 2025) (Figure 3).

In 2026, a larger share of SNPs than plans for other Medicare beneficiaries offer their enrollees transportation benefits for medical needs (67% for SNPs vs 24% for individual plans), an allowance for over-the-counter items (94% for SNPs vs 66% for individual plans), bathroom safety devices (47% for SNPs vs 21% for individual plans), in-home support services (25% for SNPs vs 7% for individual plans), and caregiver support (16% for SNPs vs 5% for individual plans). A smaller share of SNPs than individual plans offer their enrollees acupuncture (28% vs 34%) and fitness benefits (86% vs 93%).

Availability of a Part B Rebate

Both Medicare Advantage enrollees and traditional Medicare beneficiaries pay a monthly Part B premium, which will be $202.90 per month in 2026. Medicare Advantage plans may use the rebate portion of their payments from CMS to reduce the Part B and/or Part D premium. In 2026, nearly one-third (32%) of individual Medicare Advantage plans available for general enrollment will offer some reduction in the Part B premium (or a “Part B Rebate”), the same as the share in 2025, while more than two-thirds (68%) will not offer this benefit (Figure 4).

Among plans that are offering a monthly reduction in the Part B premium, more than a third (36%) are offering a monthly reduction of $100 or more (vs 28% in 2025), 23% are offering a reduction of $50.01 to $100 (vs 25% in 2025), 13% are offering a reduction of $10.01 to $50 (vs 17% in 2025), and 28% are offering a monthly reduction of $10 or less (vs 30% in 2025).

A smaller share of SNPs than individual plans offer a Part B rebate (19% vs 32%). The share of SNPs offering the Part B rebate has declined in 2026 compared with 2025 (19% vs 28%) (Figure 3). In 2026, about half (51%) of SNPs offering the Part B rebate are plans for people who are dually eligible for Medicare and Medicaid (D-SNPs), 39% are plans for people with certain chronic conditions (C-SNPs), and 10% are institutional-SNPs. Although SNPs may offer a Part B rebate, for dual-eligible individuals enrolled in the Medicare Savings Programs, which comprise most enrollment in SNPs, the rebate is paid to the state rather than to the individual because the state Medicaid program pays the Part B premium for these beneficiaries. (Note that the Medicare Savings Programs are not available in Puerto Rico.)

Availability of Special Supplemental Benefits for the Chronically Ill (SSBCI)

Beginning in 2020, Medicare Advantage plans have also been able to offer extra benefits to a subset of a plan’s enrollees, that are not primarily health related and are specifically for chronically ill beneficiaries, known as Special Supplemental Benefits for the Chronically Ill (SSBCI). In prior years, Medicare Advantage plans could also participate in the Value-Based Insurance Design Model, which allowed plans to offer these non-primarily health related supplemental benefits to their enrollees using different eligibility criteria than required for SSBCI, including offering them based on an enrollee’s socioeconomic status. However, this model was terminated at the end of the 2025 plan year.

Most individual and SNP Medicare Advantage plans still do not offer these benefits, though more SNP plans generally offer these benefits, particularly food and produce. SSBCI benefits offered in 2026 include food and produce (11% for individual plans and 85% for SNPs), general supports for living (e.g., housing, utilities) (8% for individual plans and 72% for SNPs), transportation for non-medical needs (5% for individual plans and 37% for SNPs), and pest control (3% for individual plans and 23% for SNPs) (Figure 5).

Like for other types of supplemental benefits, the scope of services for SSBCI benefits varies. For example, many plans offer a specified dollar amount that enrollees can use toward a variety of benefits, such as food and produce, utility bills, rent assistance, and transportation for non-medical needs, among others. This dollar amount is often loaded onto a flex card or spending card that can be used at participating stores and retailers, which can vary depending on the vendor administering the benefit. Depending on the plan, this may be a monthly allowance that expires at the end of each month or rolls over month to month until the end of the year, when any unused amount expires.

Methods

This analysis focuses on the Medicare Advantage marketplace in 2026 and trends over time. Data on Medicare Advantage plan availability, enrollment, and premiums were collected from a set of data files released by the Centers for Medicare & Medicaid Services (CMS):

- Medicare Advantage plan landscape files, released each fall prior to the annual enrollment period- Medicare Advantage plan crosswalk files, released each fall

- Medicare Advantage contract/plan/state/county level enrollment files, released on a monthly basis

- Medicare Advantage plan benefit package files, released quarterly

- Medicare Enrollment Dashboard files, released on a monthly basis

Connecticut is excluded from the Access to Medicare Advantage Plans with Extra Benefits section of this analysis due to a change in FIPS codes that are in the Medicare Enrollment Dashboard data but are not yet reflected in the Medicare Advantage enrollment data. Some Alaskan counties are also excluded due to differences in FIPS codes.

In previous years, KFF had calculated the share of Medicare beneficiaries enrolled in Medicare Advantage by including Medicare beneficiaries with either Part A and/or B coverage. We modified our approach in 2022 to estimate the share enrolled among beneficiaries eligible for Medicare Advantage who have both Medicare Part A and Medicare B. These changes are reflected in all data displayed trending back to 2010.

Additionally, in previous years, KFF had used the term Medicare Advantage to refer to Medicare Advantage plans as well as other types of private plans, including cost plans, PACE plans, and HCPPs. However, cost plans, PACE plans, HCPPs are excluded from this analysis in addition to MMPs. These exclusions are reflected in all data displayed trending back to 2010.

KFF’s plan counts may be lower than those reported by CMS and others because KFF uses overall plan counts and not plan segments. Segments generally permit a Medicare Advantage organization to offer the “same” local plan, but may vary supplemental benefits, premium and cost sharing in different service areas (generally non-overlapping counties).

Meredith Freed, Nancy Ochieng, Jeannie Fuglesten Biniek, and Tricia Neuman are with KFF. Anthony Damico is an independent consultant.